This comprehensive report examines New Drywall Installation Projects In Massachusetts through extensive research and analysis.

Key Research Takeaways

- Comprehensive Analysis: This report covers all major aspects of New Drywall Installation Projects In Massachusetts

1. Executive Summary

Massachusetts’ construction landscape, and specifically its drywall installation sector, is currently navigating a complex confluence of soaring housing demand, persistent labor shortages, escalating material costs, and unprecedented opportunities for innovation. The state faces a critical need for approximately 220,000 new homes by the early 2030s to address its severe housing shortfall, yet building activity severely lags the national average, ranking as the 6th lowest among U.S. states in per capita housing permits issued[5]. While Massachusetts has seen a notable surge in housing development between 2020 and mid-2025, adding roughly 97,656 net housing units, with 71,135 of those in Greater Boston, this progress remains insufficient to curb high prices and out-migration[9]. This executive summary provides a high-level overview of these dynamics, highlighting key challenges, trends, and strategic opportunities for the drywall installation industry within the broader Massachusetts construction and housing market.

Massachusetts Construction Boom Falls Short of Housing Needs

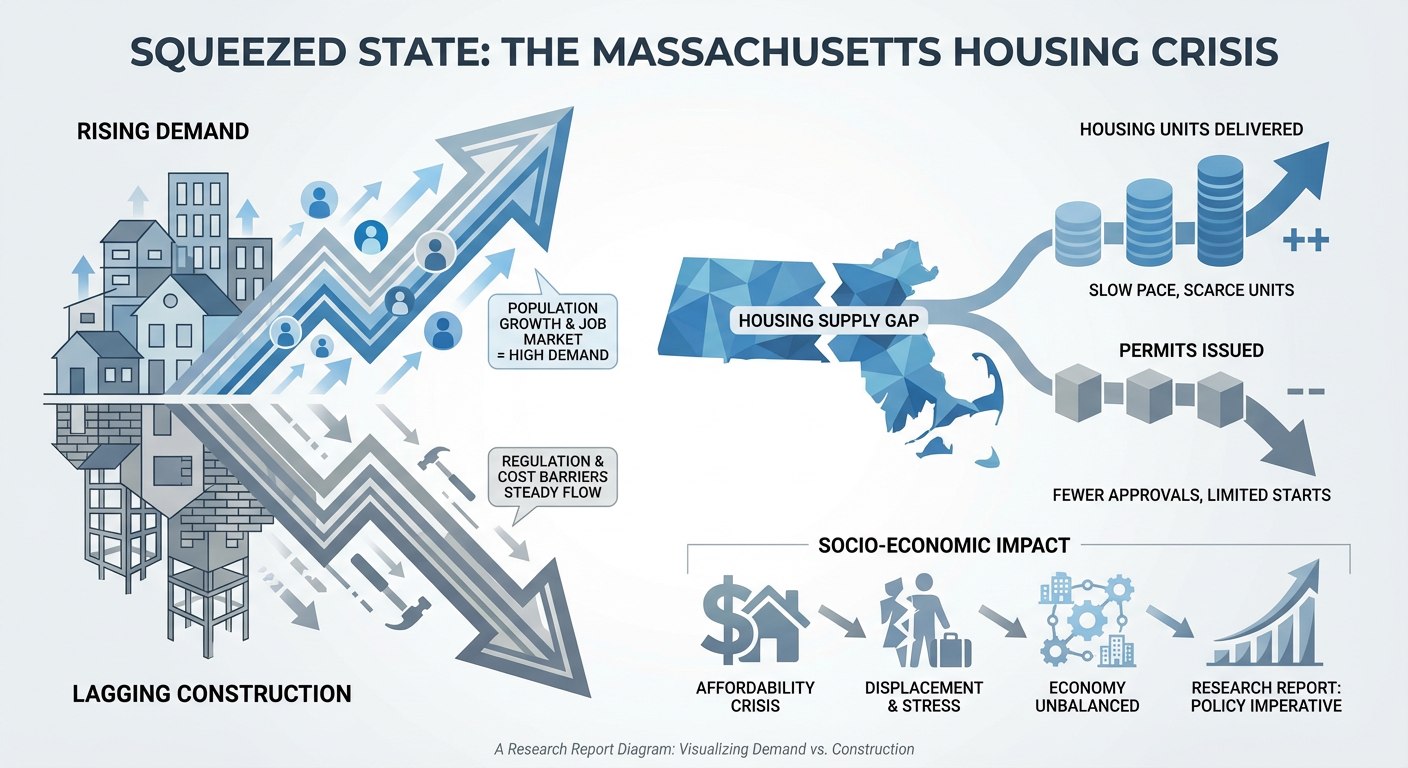

The imperative for new housing in Massachusetts is undeniable, yet the state’s construction output consistently falls short of ambitious targets. State leaders estimate a need for approximately 22,000 new homes annually through 2035, totaling 222,000 homes, to meet demand and alleviate the ongoing housing crisis[2]. However, the state’s current pace of development, despite a recent uptick, barely scratches the surface of this requirement. From April 2020 to July 2025, Massachusetts managed to add 97,656 housing units, with the majority (71,135 units) concentrated in the Greater Boston area[9]. This represents a significant expansion compared to previous decades but translates to an average annual addition of roughly 19,000 units per year, still below the estimated need.

The disparity between demand and supply is further underscored by permitting rates. In 2024, Massachusetts issued only 14,338 residential building permits, equating to about 201 permits per 100,000 residents[5]. This figure is significantly lower than the U.S. national average of 281 permits per 100,000 residents, placing Massachusetts among the bottom ten states nationally in per capita housing production[5]. Neighbouring states like New Hampshire and Maine, for instance, permitted nearly twice as many units per capita, illustrating Massachusetts’ relative slowdown in building activity[2]. This chronic under-building has exacerbated housing inventory shortages, fueling some of the highest rents and home prices in the nation. The median price of a newly built home in Massachusetts topped $1 million in 2024, a direct consequence of constrained supply and elevated construction costs[10].

The geographic distribution of recent construction has also been uneven. While Greater Boston has absorbed the bulk of new developments, with its housing stock expanding by 5-6%[9], many suburban and rural areas have seen minimal growth. This regional imbalance forces significant commutes and concentrates housing pressures in urban centers. The consequences of this shortfall extend beyond mere housing affordability, impacting the state’s economic competitiveness. High housing costs make it challenging for companies to attract and retain talent, leading to out-migration of young families and hindering overall economic growth[9].

To address this critical situation, Massachusetts has begun implementing significant policy responses. Governor Maura Healey’s administration enacted the $5+ billion Affordable Homes Act in 2024, designed to spur development through zoning reform and direct funding[5]. Within 18 months of its passage, this act is credited with initiating 90,400 housing units (built, under construction, or permitted), indicating an encouraging upward trend in building starts[5]. Additionally, the MBTA Communities Law mandates denser housing near transit hubs in many suburbs, challenging traditional zoning barriers. These policy efforts demonstrate a commitment to “bending the curve” on housing production, yet state officials and industry stakeholders acknowledge that bureaucratic hurdles, including lengthy and complex approval processes, continue to impede progress. To truly close the housing gap, Massachusetts will require sustained, historic levels of construction activity, coupled with diligent efforts to streamline permitting and incentivize development.

Workforce Shortages and High Labor Costs Slow Projects

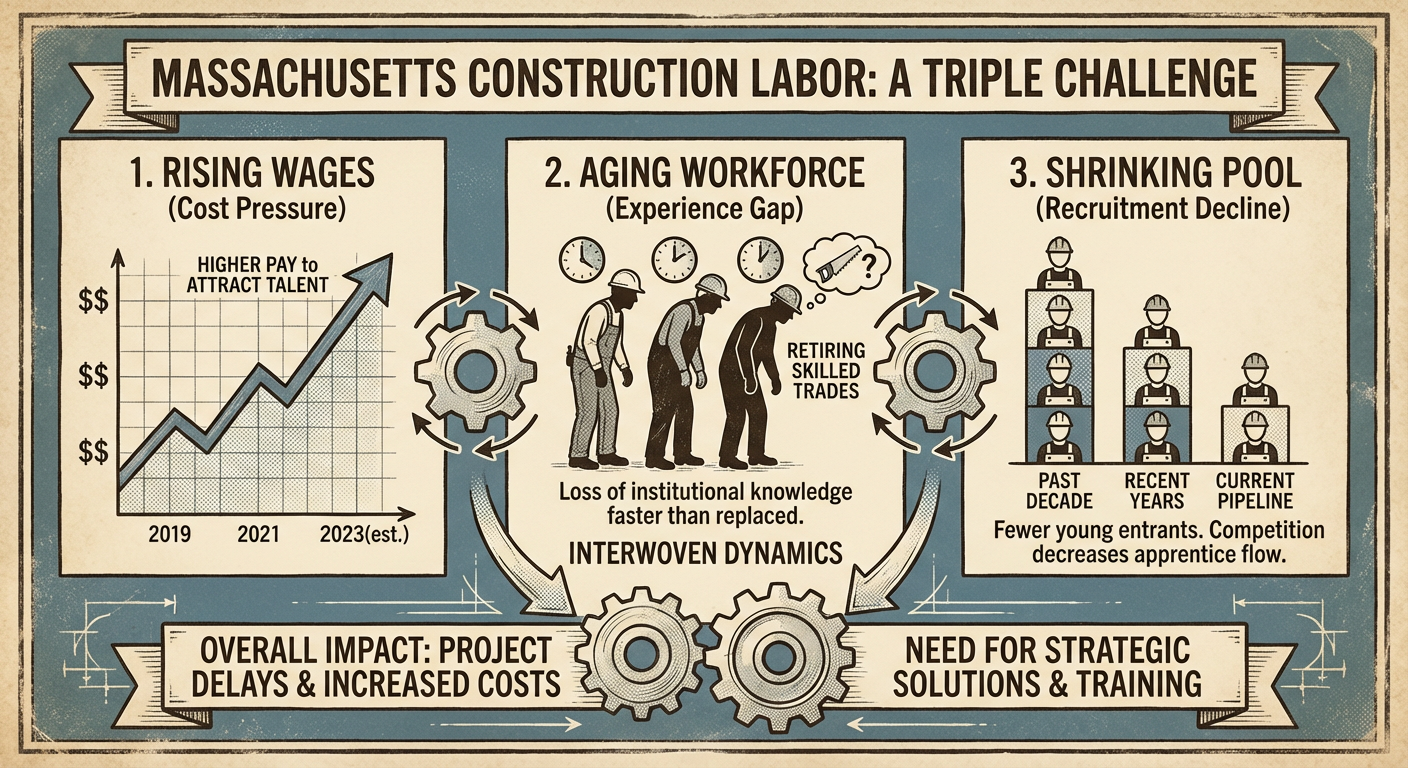

The ambitious goals for housing and infrastructure development in Massachusetts are significantly hampered by a severe and persistent labor shortage across the construction industry. This scarcity affects all trades, including critical roles like drywall installers, carpenters, and electricians. Unemployment in the state’s construction sector reached a remarkably low 2.5% in June 2024, the lowest June rate in over 17 years[7]. This figure signifies a state of near full employment, an unusual condition for an industry typically characterized by cyclical fluctuations.

The Associated General Contractors (AGC) reported that a staggering 94% of U.S. construction firms struggled to fill open positions in 2024, a national trend acutely felt in Massachusetts[6]. Of these, 28% of contractors had at least 11 unfilled craft positions, contributing to chronic gaps in core site labor[6]. This acute scarcity directly impacts project timelines and costs. A substantial 54% of contractors reported project delays attributable to workforce shortages in the past year, making labor availability a more significant bottleneck than even material supply chain issues[6]. For drywall contractors, this means that even with materials readily available, projects can stall if there aren’t enough skilled hands to hang and finish the walls, creating ripple effects that delay subsequent trades.

The intense competition for scarce labor has inevitably driven up wages. Massachusetts now boasts the highest average hourly construction wage in the nation, reaching approximately $48.90 as of early 2024, far exceeding the U.S. average of $37.70[3]. These wages have been consistently rising, with year-over-year increases of around 5%[3]. While beneficial for workers, these high labor costs add considerable pressure to project budgets. Given that labor can account for 40-50% of drywall installation costs, these increases directly impact bid prices and developer margins. Consequently, Boston’s construction costs are among the highest globally, a factor directly linked to the robust wage environment.

A fundamental cause of this labor crunch is a demographic shift: an aging workforce with insufficient new entrants. Approximately 30% of residential construction workers in Massachusetts were aged 55 or older in 2023, and the number of workers over 50 has doubled in recent years, while the share of young workers (under 25) has plummeted[2][7]. This demographic cliff means that within the next decade, a significant portion of the experienced workforce will retire, further exacerbating the shortage. The decline in vocational training and the societal push towards college education over skilled trades have created a “missing generation” of tradespeople. Efforts are now underway to reverse this trend, with unions expanding apprenticeship programs and industry organizations highlighting the attractive wage premiums in Massachusetts’ construction sector to draw new talent[2][3]. Immigration also plays a crucial role, with about 21% of Massachusetts construction workers being non-U.S. citizens, indicating a substantial reliance on foreign-born labor, particularly in trades like roofing and masonry where over 50% are non-citizens[2]. This reliance makes the industry highly vulnerable to shifts in immigration policy.

For stakeholders, the labor crisis translates into higher project bids, longer timelines, and the need for significant contingency planning. Developers must account for potential wage escalation clauses and incentives to retain skilled crews. While the demand for workers creates opportunities for current tradespeople, it also places immense strain on existing crews, leading to potential overwork and safety concerns. The challenge for Massachusetts’ construction industry is to innovate and adapt, either by enhancing productivity through technology and improved management or by aggressively expanding the talent pipeline. The success of future drywall installation projects across the state will largely hinge on how effectively these labor challenges are addressed.

Rising Costs Squeeze Project Viability (Materials, Financing & Delays)

The viability of drywall installation projects in Massachusetts is increasingly challenged by a persistent rise in overall construction costs, coupled with evolving financial landscapes and project delays. The period between 2020 and 2022 saw dramatic inflation in building material prices, largely driven by pandemic-induced supply chain disruptions and heightened demand. Gypsum wallboard, a core component of drywall installation, experienced a staggering 44.6% increase in its Producer Price Index over just two years[4]. This was part of a broader trend where residential construction input costs climbed approximately 17% annually in 2021-2022[4]. Although 2023 brought some stabilization, with gypsum prices declining by 2.0% and overall material costs rising only 1-2%, prices remain significantly above pre-pandemic levels[4]. This volatility forces contractors to contend with unstable pricing, material backorders, and the necessity of sourcing alternative products, all of which complicate budgeting and risk management.

Trade tariffs have further contributed to cost escalation. Duties of up to 39.5% on Canadian lumber, critical for framing, and 25% on steel, have consistently added an estimated $7,500 to $10,000 to the cost of a new single-family home. Given that roughly 7.3% of all U.S. homebuilding materials are imported, these tariffs exert a considerable multiplier effect on overall project expenses[10]. In Massachusetts, already one of the most expensive states for construction, these tariffs deepen the financial strain on developers. They either absorb these added costs, compress profit margins, or pass them on to consumers, further impacting housing affordability.

Perhaps the most significant economic headwind impacting project viability has been the rapid increase in interest rates since 2022. Higher financing costs for development loans disproportionately affect projects with tight margins, rendering many previously viable ventures financially unfeasible. A prominent example is the Suffolk Downs redevelopment in East Boston, an ambitious project envisioning 10,000 housing units. Its developers, HYM Investment Group, announced a significant slowdown in mid-2023, indefinitely postponing subsequent phases of the $9.6 billion plan due to rising interest rates and construction costs[11]. Only 475 apartments, a fraction of the total, are proceeding as initially planned. Similarly, the robust life sciences sector, a major driver of construction in Massachusetts, experienced setbacks, with Pfizer canceling plans for a 270,000 sq. ft. facility in Everett due to viability concerns in a high-interest-rate environment[11]. These instances highlight how capital market conditions can abruptly freeze project pipelines, directly curtailing future drywall installation volumes.

These financial pressures, combined with labor shortages, lead to significant project delays and increased uncertainty. Lead times for crucial equipment, such as electrical switchgear panels (up to 48 weeks) and HVAC systems, cause cascading hold-ups that extend project timelines. Nationwide, nearly 30% of construction projects faced significant delays or indefinite holds in late 2023[11], a trend mirrored in Massachusetts. Delays mean higher overhead costs for contractors, deferred revenue for owners, and increased risk throughout the project lifecycle. Developers are increasingly negotiating price escalation clauses in contracts to mitigate risk, a practice uncommon before the recent volatility. The median price of a new condo in Greater Boston has reached record highs in 2024, demonstrating how these cumulative costs are ultimately transferred to the end-user. Moving forward, robust risk management, value engineering, and potentially innovative procurement strategies will be essential to ensure project feasibility in this challenging economic climate.

Innovative Construction Methods Gain Traction Amid Labor and Time Pressures

The confluence of severe labor shortages, high costs, and urgent housing demand is compelling the Massachusetts construction industry to explore and adopt innovative construction methods, particularly accelerated building techniques. While traditionally slow to embrace change, developers are increasingly looking towards prefabrication and modular construction as viable solutions to enhance efficiency and accelerate project delivery.

Modular construction, which involves manufacturing components or entire volumetric units in a factory setting before assembly on-site, offers significant advantages. These include year-round production shielded from weather delays, assembly-line precision, and reduced on-site labor hours due to automation and streamlined processes. Although modular methods represent only about 2% of new construction in Massachusetts, interest is steadily growing[8]. Countries like Sweden, Germany, and Japan have much higher adoption rates, with prefab housing accounting for 26% of the German market, demonstrating its proven efficacy in addressing housing needs[13].

A compelling regional demonstration of modular construction’s potential occurred in West Swanzey, New Hampshire, just across the Massachusetts border. In early 2023, an 84-unit affordable apartment complex utilized volumetric modular units, manufactured in a Pennsylvania factory and then transported to the site. The project progressed from foundation work in February to approximately 80% completion by May, effectively building a large residential complex within 2.5 months[8]. This rapid timeline, virtually unachievable with traditional stick-built methods, translates directly into lower financing costs and faster revenue generation for developers. Massachusetts housing officials are actively studying such projects as a model for accelerating their own housing mandates.

Beyond full modular builds, panelized construction is gaining traction. This involves fabricating wall, floor, and roof panels with framing, and sometimes insulation or sheathing, in a controlled environment. Once on-site, these panels are quickly erected using cranes by smaller crews. Studies indicate that using prefabricated wall panels can reduce on-site framing labor time by approximately 71% for a typical home, a crucial efficiency gain in a tight labor market[14]. For the drywall industry, this innovation could extend to pre-rocked wall panels, where drywall is factory-attached, requiring only tape and finishing on-site. This approach minimizes on-site cutting waste, improves precision, and reduces the need for extensive scaffolding, further boosting productivity. Regional firms like KBS Builders in Maine are actively marketing these solutions to Massachusetts developers, promising reduced lead times and more predictable costs.

| Feature | Traditional (Stick-Built) | Modular/Prefabricated | Implication for Drywall Inst. |

|---|---|---|---|

| Construction Time | Longer, weather-dependent | Significantly shorter (20-50% reduction) | Faster job cycles, less on-site scope (more factory work) |

| On-Site Labor Needs | High, skilled trades | Lower on-site, more factory-based | Shift of work, specialization in factory vs. field |

| Quality Control | Variable, site-dependent | Consistent, factory-controlled | Improved finish consistency, fewer defects |

| Material Waste | Higher (due to on-site cutting) | Lower (optimized factory cuts) | Reduced scrap, easier compliance with MA waste bans |

| Cost Factors | Volatile, interest rate sensitive | More predictable, time-cost savings | Different cost structure for drywall firms (logistics, factory) |

| Weather Impact | Significant delays possible | Minimal, factory work unhindered | More reliable scheduling for completion |

Technological advancements are also transforming traditional drywall installation on job sites. Contractors are investing in automated taping and finishing tools that significantly accelerate joint compound application, laser-guided layout systems for precise framing, and ergonomic lifting equipment to minimize physical strain. While fully robotic drywall installation remains largely experimental, these innovations can boost productivity by 20-30% in finishing stages. Building Information Modeling (BIM) and digital project management further streamline coordination, reducing conflicts and rework. Massachusetts’ forward-thinking commercial builders, particularly in the tech-savvy Boston market, are early adopters, leveraging these tools to mitigate labor shortages.

Despite the clear benefits, widespread adoption of modular and prefabricated methods in Massachusetts faces hurdles. These include initial skepticism regarding quality control and a lack of local modular manufacturing capacity. Concerns about quality arose from past incidents, though modern modular construction has made significant strides in this area[8]. The high upfront costs of establishing modular factories and the logistical challenges of transporting large modules across state lines (e.g., from Pennsylvania to Massachusetts) also hinder adoption. Additionally, traditional building codes and inspection processes historically posed challenges for modular projects, although Massachusetts has been updating regulations to be more accommodating. Future progress may involve hybrid approaches, combining traditional building with modular components like prefabricated bathroom pods, to selectively leverage efficiency gains where most impactful. The pressure to “build more with less” and increase speed is pushing the drywall industry to innovate significantly, with off-site fabrication poised to become a game-changer for certain market segments, ultimately reshaping how drywall is installed in Massachusetts.

Changing Industry Practices and Case Lessons in Massachusetts Drywall Projects

The intense pressures of cost control and project deadlines in Massachusetts’ construction sector have inadvertently fostered some concerning labor practices, particularly evident in residential drywall installation. A 2024 investigation by the UMass Amherst Labor Center shed light on a “new business model” wherein mid-sized drywall and framing subcontractors increasingly bypass direct employment by utilizing labor brokers[1]. These brokers, often operating without proper legal frameworks, supply low-paid and frequently undocumented worker crews who are often engaged in wage theft and worker misclassification. This practice allows unethical contractors to undercut bids by saving significantly on payroll taxes, overtime, and benefits, putting ethical competitors at a severe disadvantage[1].

A stark example of this issue is the North Square Apartments development in Amherst (2018-2019). The project’s drywall work was subcontracted to Combat Drywall Inc., a Billerica firm, which then further sub-subcontracted to a labor broker known as “Poncho.” This arrangement led to dozens of migrant workers performing drywall installation for weeks without being paid, or being underpaid, with overtime laws routinely ignored. The situation only came to light and was partially resolved after intervention by a local carpenters’ union organizer[1]. This case, which UMass researchers termed a “tragedy,” prompted increased scrutiny from state authorities, with the Attorney General’s office subsequently fining Combat Drywall for wage violations. It also galvanized support for legislation imposing joint liability on general contractors for subcontractor wage theft, emphasizing the need for greater due diligence from primary builders.

Massachusetts’ construction market historically operates within a dual union and non-union framework. Commercial projects, especially in Greater Boston, are largely unionized, ensuring higher wages and robust apprenticeship programs. Drywall installers working under union agreements (e.g., through carpenters’ or painters’ unions) often command higher pay and benefit from comprehensive training but can contribute to higher project costs. Non-union firms, particularly in residential and smaller commercial sectors, offer more flexible arrangements and aim for tighter margins. However, the current labor shortage has somewhat blurred these lines; non-union companies are often compelled to raise wages and benefits closer to union levels to attract and retain workers[3]. This tight market has even seen union halls temporarily dispatching workers to open-shop projects when no other labor is available. This evolving dynamic highlights a crucial industry crossroads: either risk further entrenchment in a low-wage underground economy for some sectors or commit to formal training, fair wages, and proper hiring practices to ensure sustainable growth.

Maintaining safety and quality remains a significant challenge within this demanding environment. Massachusetts’ stringent building codes, particularly for fire-rated drywall assemblies, and a strong OSHA presence, mandate high standards. However, accelerated timelines and stretched workforces can create pressures for shortcuts. Instances of drywall failures due to improper fastening, though rare, underscore the critical importance of meticulous installation. Many firms are now implementing enhanced quality assurance protocols, including digital tools for logging and reviewing work, to maintain standards. Safety, especially concerning the lifting of heavy drywall sheets and fall protection, is also paramount, particularly with an aging workforce. Industry associations are increasing training specific to drywall tasks, and some firms, like Kaplan Construction, have received awards for their adaptive safety practices, demonstrating a commitment to mitigating risks[6]. These efforts are crucial to prevent costly rework, accidents, and reputational damage.

Furthermore, new drywall installation projects are increasingly subject to environmental considerations. Massachusetts’ strict waste bans, in place since 2006, prohibit clean gypsum drywall off-cuts from landfills, mandating recycling[15]. This encourages the adoption of precise fabrication and waste reduction strategies, such as closed-loop drywall recycling programs where scrap is processed into new materials. There is also growing interest in alternative wall systems like magnesium oxide (MgO) boards or hemp-based panels, offering lower environmental impacts, particularly in green building projects. The confluence of these changing practices—from labor procurement to quality control and environmental stewardship—means that drywall contractors in Massachusetts must navigate a complex regulatory and ethical landscape. Forward-thinking firms that embrace transparency, fair labor, and sustainable practices will be best positioned for long-term success and competitive advantage within this evolving market.

Notable Examples

To illustrate the multifaceted challenges and opportunities within Massachusetts’ drywall installation sector, several notable projects serve as key case studies:

- North Square Apartments, Amherst (2018–2019) – Wage Theft in a Drywall Subcontract: This 130-unit affordable housing development became a stark illustration of illicit labor practices. The main contractor, Keith Construction, awarded the drywall work to Combat Drywall Inc. from Billerica. Combat Drywall, with only two registered employees, then sub-subcontracted the entire drywall hanging operation to an informal labor broker. This arrangement resulted in widespread wage theft, with migrant workers going unpaid for weeks and being denied overtime. Intervention by a carpenters’ union organizer eventually led to the recovery of some owed wages. The UMass Amherst Labor Center highlighted this as a “tragedy” and a prime example of a “new business model” built on worker misclassification. The incident spurred legislative efforts in Massachusetts to hold general contractors jointly liable for subcontractor wage theft, underscoring the critical need for due diligence in the supply chain and ethical labor practices[1].

- Suffolk Downs Redevelopment, East Boston (2023 pause) – Mega-Project Stalled by Market Conditions: Envisioned as a $9.6 billion, 10,000-unit mixed-use development, Suffolk Downs epitomized Massachusetts’ ambition to tackle its housing crisis. However, in mid-2023, developer HYM Investment Group announced a significant slowdown of future phases due to soaring interest rates and construction costs. Only 475 apartments from the initial phase proceeded on schedule, with the majority of the planned development indefinitely postponed. This case vividly demonstrates how even large-scale projects with high public support can become financially unviable in adverse economic conditions. For the drywall industry, this meant the sudden loss or delay of thousands of potential installation jobs, highlighting the sensitivity of construction pipelines to capital market fluctuations and the necessity for developers and contractors to plan for economic volatility[11].

- West Swanzey Modular Housing, New Hampshire (2023) – Speedy Construction via Modular Techniques: Just across the state border, the 84-unit West Swanzey Apartments showcased the transformative potential of modular construction. Modules, with walls, wiring, plumbing, and even much of the drywall and finishes pre-installed, were manufactured in a Pennsylvania factory and assembled on-site. The project progressed from ground-breaking in February to 80% completion by May, delivering affordable housing in roughly half the time of traditional methods. This success story demonstrated to Massachusetts officials and developers how off-site fabrication can significantly accelerate project delivery, reduce on-site labor requirements, and offer cost predictability. It underscores the growing importance of innovation in construction methods to address housing needs rapidly, signaling a potential shift towards more factory-based drywall work in the future for certain project types[8].

- Takeda Cambridge Lab Build (2022–2026) – Major Biotech Construction Driving Drywall Demand: In contrast to residential and general commercial projects sensitive to economic shifts, Takeda’s 16-story, 600,000 sq. ft. R&D center in Kendall Square, Cambridge, exemplifies the resilience of Massachusetts’ life sciences sector. This project, part of the region’s $11.7 billion in active biotech construction, involves extensive and specialized drywall installation, meeting stringent requirements for sound damping, fire-rating (Type X drywall), and cleanroom environments[12]. The project has proceeded steadily, employing hundreds of union tradespeople. This example highlights how sector-specific demand, particularly from well-capitalized clients in critical industries, can buffer the construction market against broader economic headwinds. It also emphasizes the opportunity for drywall contractors capable of handling advanced specifications and complex lab build-outs.

These examples collectively illustrate the core themes impacting drywall installation projects in Massachusetts: the urgent housing need, the chronic labor scarcity, the volatility of costs and financing, and the pressing demand for innovation and ethical practices. The future success of this sector will depend on its ability to adapt strategically to these powerful forces. The next section will delve deeper into the specific market size and growth projections for drywall installation projects in Massachusetts, providing quantitative data to further ground this executive overview.

2. Massachusetts Housing Shortfall and Construction Activity

Massachusetts, a state renowned for its innovation economy, prestigious universities, and vibrant cultural scene, finds itself in the throes of a profound housing crisis. This crisis is characterized by a significant and persistent gap between the burgeoning demand for housing and the state’s lagging construction rates. The implications extend far beyond mere shelter, impacting economic competitiveness, social equity, and the overall quality of life for its residents. This section will meticulously examine the various facets of Massachusetts’ housing shortfall, delving into housing unit production, permitting trends, the socio-economic ramifications of the affordability crisis, and the multifaceted challenges confronting the construction industry in its efforts to bridge this critical gap. Understanding these dynamics is paramount for anyone involved in the state’s building industry, including drywall installation professionals, as they directly influence project pipelines, labor availability, and material costs.

2.1 The Persistent Housing Production Gap and Its Socio-Economic Impacts

Massachusetts faces an acute housing shortage that has been decades in the making. State planning estimates project a need for approximately **220,000 new homes by the early 2030s** to adequately meet demand and stabilize the market [1]. This translates to an annual production target of roughly **22,000 units per year** through 2035 [23]. However, historical building activity has consistently fallen short of these ambitious targets. Between 2010 and 2020, the state averaged only **19,000 units per year** [24], a pace that promises to leave Massachusetts tens of thousands of units short of its goal if not substantially accelerated. Recent efforts have shown some progress, with Massachusetts adding an estimated **97,656 net housing units** from April 2020 to July 2025 [19]. Notably, a significant portion of this growth, **71,135 units**, occurred within the Greater Boston area [19], marking the largest five-year expansion of metro Boston’s housing base in decades [19]. This positive trend was bolstered by the state’s 2024 Affordable Homes Act, which, within 18 months of its passage, helped kick-start **90,400 housing units** (either built, under construction, or permitted) [18]. Yet, despite this recent surge, the overall pace of new construction remains “insufficient” to curb high prices and out-migration [4]. A stark illustration of this under-building is found in residential permitting data. In 2024, Massachusetts issued only **14,338 housing permits** [2], equating to merely **201 permits per 100,000 residents** [2]. This figure positions Massachusetts as having the **6th lowest per capita permitting rate nationally**, significantly trailing the U.S. average of **281 permits per 100,000 residents** [2]. To put this into further perspective, neighboring states like New Hampshire and Maine permitted roughly double the units per capita [26], underscoring Massachusetts’ relative slowdown in housing production. This persistent lag in construction compared to demand has profound socio-economic consequences: * **Soaring Housing Costs:** The most immediate effect is the escalation of both rental and home purchase prices. With limited supply and robust demand, Massachusetts consistently ranks among the most expensive housing markets in the nation. The median price of a newly built home in Massachusetts topped **$1 million in 2024** [39]. This makes homeownership unattainable for many and forces a significant portion of income towards housing for renters. * **Out-migration and Talent Retention Challenges:** High housing costs directly contribute to a phenomenon of “out-migration,” particularly among young families seeking more affordable living conditions elsewhere [5]. This exodus poses a serious threat to the state’s economic vitality, as businesses struggle to attract and retain talent when prospective employees cannot find affordable places to live [5]. As a result, Massachusetts’ competitive edge in critical sectors like technology and biopharma is undermined. * **Economic Inequality and Social Stratification:** The housing crisis exacerbates existing economic inequalities. Lower-income households and essential workers are disproportionately affected, often forced into longer commutes or substandard living conditions. This creates a deeply stratified society where access to opportunity is increasingly tied to housing affordability. * **Regional Disparities:** While Greater Boston has seen the lion’s share of recent housing development (71,135 of the 97,656 new units) [19], many suburbs and rural towns have added very few homes. This geographic imbalance concentrates growth—and its associated pressures—in already dense urban areas, while distant communities fail to contribute to overall housing supply. This perpetuates long commutes and limits housing options for a diverse workforce [44]. * **Reduced Disposable Income:** The high burden of housing costs reduces the disposable income of residents, which in turn limits consumer spending on other goods and services. This can dampen local economic growth and make it difficult for other sectors to thrive. In response to these challenges, Massachusetts policymakers have initiated several measures. The previously mentioned Affordable Homes Act and recent zoning reforms, like the MBTA Communities Law (requiring denser housing near transit), aim to accelerate housing production [47]. While these efforts are beginning to “bend the curve” [47], the state must overcome significant regulatory hurdles, including lengthy approval processes, to truly meet its ambitious housing targets. The sheer scale of the housing shortfall demands sustained, historic levels of construction activity, alongside innovative solutions to address underlying cost and labor constraints.

2.2 Construction Workforce Dynamics: Shortages, Wages, and Eroding Practices

The ability of Massachusetts to address its housing shortfall is fundamentally constrained by the state of its construction workforce. While overall construction employment in Massachusetts has grown significantly post-recession, reaching **172,500 workers in 2023** (up from ~138,000 in 2012) [27], and specialized trades saw a **53% growth** over the same period [29], the industry is simultaneously battling a severe labor shortage, an aging workforce, and challenges related to labor practices.

2.2.1 The Critical Labor Shortage and Skyrocketing Wages

The most pressing issue is the acute and widespread scarcity of skilled labor. In June 2024, the construction unemployment rate in Massachusetts plummeted to a mere **2.5%** [8], the lowest June level in over 17 years [8]. This figure essentially represents full employment in a sector that typically experiences higher cyclical unemployment. A national survey in 2024 revealed that **94% of U.S. construction firms** struggled to fill open positions [6], with Massachusetts being no exception. Many firms reported having at least **11 unfilled craft positions** (e.g., carpenters, drywall hangers, plumbers) [33], indicating a chronic deficit in core trades – the very people needed for new drywall installations. This profound imbalance between labor supply and demand has directly driven up wages, making Massachusetts home to some of the highest construction pay in the U.S. By early 2024, the state’s average hourly construction wage reached an unprecedented **$48.90** [9]. This figure far outstrips the national average of approximately $37.70 [9] and represents annual wage increases of around 5% [36]. While beneficial for workers, these escalating labor costs significantly impact project budgets. For drywall contractors, where labor can constitute 40-50% of total costs, these wage hikes either squeeze profit margins or necessitate higher project bids. “Lucey said he has seen project costs come in 25% or 30% higher than he expected a year ago across a variety of housing types,” due in part to labor costs [49]. This contributes to Boston’s reputation as having some of the highest construction costs globally. The immediate consequence of this labor scarcity and high wage environment is project delays. A significant **54% of contractors reported project delays due to workforce shortages** in the past year, making it a more prevalent cause of setbacks than even supply-chain issues [7]. This means that even when materials are available, a lack of skilled installers can halt progress and extend timelines for drywall and other critical trades. Moreover, some subcontractors in the busy Boston market are reportedly turning down new work due to insufficient crews [51], creating a bottleneck for new construction.

2.2.2 Aging Workforce and Talent Pipeline Challenges

A fundamental cause of the current labor crisis is demographic. Massachusetts’ construction labor force is rapidly aging, with approximately **30% of residential construction workers aged 55 or older** as of 2023 [30]. Industry leaders note that the number of workers over 50 has “doubled” in recent years, while the share of young workers under 25 has “dropped dramatically” [10]. This demographic shift portends a significant wave of retirements, with potentially “one in three skilled workers” retiring within the next decade [43]. The lack of new entrants into the trades over recent decades means the talent pipeline is insufficient to replace these retiring workers, let alone meet growing demand. Efforts are underway to address this: unions have expanded apprenticeship programs, and the high wages in Massachusetts construction may attract more individuals to vocational training. Policy reforms aim to address a “missing generation” of skilled workers by promoting construction careers earlier in education.

2.2.3 Reliance on Immigrant Labor and Eroding Practices

Foreign-born workers constitute a crucial segment of Massachusetts’ construction workforce, particularly in certain trades. In 2023, around **21% of construction laborers in the state were not U.S. citizens** [34], which is more than double their 10% share in the overall labor force [34]. This reliance is even higher in specific trades like roofing and masonry, where over **50% of workers are non-citizens** [35]. This makes the industry exceptionally vulnerable to shifts in immigration policy, as strict visa limits or enforcement crackdowns could further exacerbate labor shortages [37]. Compounding these challenges, a worrying trend of “low-road” labor practices has emerged, particularly in residential construction and drywall installation. Research by the UMass Amherst Labor Center in 2024 revealed that some mid-size drywall and framing subcontractors are increasingly using **”labor brokers”** to supply crews rather than hiring employees [14]. These brokers often recruit low-paid, frequently undocumented workers, paying them in cash and circumventing critical labor protections such as payroll taxes and overtime [14]. A notable example occurred at the **North Square Apartments in Amherst** (2018-2019) [71]. A small drywall firm (Combat Drywall) subcontracted the entire installation to an informal broker, leading to widespread **wage theft** and unpaid overtime for migrant workers [14]. This case, described as a “tragedy” by UMass investigators [74], exposed an underground labor system that undercuts ethical contractors and exploits vulnerable workers. Such practices, once marginal, are now reportedly “common in non-union residential projects” [15] in Massachusetts. The Attorney General’s office has increased enforcement against wage theft and misclassification, and there are calls for legislation imposing joint liability on general contractors for subcontractor wage violations. This situation underscores a conflict within the industry: the pressure to build more affordably clashes with the imperative for fair labor standards and a sustainable workforce pipeline.

2.3 Cost Volatility: Materials, Financing, and Project Viability

Beyond labor, the Massachusetts construction landscape is characterized by significant cost volatility spanning materials, financing, and regulatory compliance. These factors collectively squeeze project viability, leading to delays, cancellations, and ultimately contributing to the housing shortfall.

2.3.1 Material Price Swings and Supply Chain Disruptions

The period from 2020 to 2022 witnessed dramatic and unpredictable spikes in building material prices, heavily impacting drywall installations. The Producer Price Index (PPI) for **gypsum building materials (drywall) surged an astonishing 44.6%** over these two years [16], among the sharpest increases on record. This volatility made accurate budgeting exceptionally challenging for contractors. While 2023 brought some reprieve, with a slight **2.0% year-over-year decrease** in gypsum prices [17], prices remain roughly **40% higher than pre-pandemic (2019) levels** [38]. Other critical materials also saw significant cost increases: * **Softwood Lumber:** Essential for framing behind drywall, lumber prices fluctuated wildly, ending 2023 still **22.7% above 2019 levels** despite a 33% two-year decline from its peak [40]. * **Ready-Mix Concrete:** Prices jumped **11.2% in 2023 alone** [41]. * **Steel, Insulation, Wiring:** These and other components saw double-digit percentage increases since 2020. These input cost surges drove overall construction cost inflation for residential projects by an average of **17% per year in 2021-2022** [42], far outstripping general inflation rates. Although material costs stabilized in 2023 (up 1-2% on average) [42], the cumulative increases mean that current projects are still priced significantly higher than pre-pandemic equivalents. Builders have passed some of these costs onto consumers, contributing to the record median price of newly built homes in Massachusetts. This directly affects the affordability equation, making it harder for new projects to “pencil out” economically.

2.3.2 Tariffs and Trade Policy Impacts

Trade policies, particularly tariffs, have added another layer of cost. Duties on imported materials such as Canadian lumber (up to 39% [12]) and steel (25% [12]) are estimated to add an additional **$7,500 to $10,000** to the cost of a typical new single-family home [11]. With approximately **7.3% of all U.S. homebuilding materials being imported** [12], these tariffs have a tangible multiplier effect on project budgets, especially in high-cost regions like Massachusetts. Developers are either forced to absorb these costs, eroding profit margins, or pass them on to homebuyers, further exacerbating affordability issues. This tariff-driven volatility also complicates procurement strategies, with some builders resorting to stockpiling materials to hedge against future price increases [45].

2.3.3 Rising Interest Rates and Project Cancellations

The rapid acceleration of interest rates since 2022 represents a significant headwind for construction. Higher borrowing costs directly increase the financial burden on developers through more expensive construction loans and decrease buyer demand due to higher mortgage rates. In Massachusetts, this has rendered many economically marginal projects, particularly high-density housing ventures with tight profit margins, financially unfeasible. A prominent example is the massive **Suffolk Downs redevelopment in East Boston**, initially planned for 10,000 housing units and a total budget exceeding $9.6 billion [13]. In mid-2023, facing escalating interest rates and construction costs, developers (HYM Investment Group) announced a significant pause, with only **475 units** proceeding as scheduled [13]. The majority of the project’s future phases were put on indefinite hold pending more favorable financing conditions [67]. Similarly, a planned **270,000 sq. ft. Pfizer research facility in Everett** was scrapped in 2023 due to viability concerns [13]. These high-profile cancellations and delays underscore how sensitive project pipelines are to capital market conditions, directly impacting current and future drywall installation volumes. Many mid-sized developments across the state have also quietly pushed back their completion dates or scaled down their ambition. Construction project abandonments nationally saw an **11% year-over-year increase by mid-2023** [46], with nearly **30% of U.S. projects experiencing significant delays or indefinite holds** in late 2023 [46]. These delays translate into higher overhead costs for contractors, deferred revenue for owners, and increased risk for all stakeholders. Lenders are demanding larger contingency buffers, and contractors are increasingly wary of fixed-price contracts in such an unpredictable environment.

2.4 Innovations and Adaptations to Overcome Challenges

Despite significant headwinds, the Massachusetts construction industry is demonstrating resilience and an increasing willingness to adopt innovative strategies to address labor shortages, cost pressures, and accelerate construction.

2.4.1 Rise of Modular and Prefabricated Construction

Facing the dual challenges of labor scarcity and the urgent need for faster development, **off-site construction techniques** are gaining traction. Modular construction, where sections of buildings or entire units are manufactured in a factory before being transported and assembled on-site, offers compelling advantages. While still nascent in Massachusetts – representing only about **2% of new construction** [8] – interest is clearly growing, particularly for affordable housing, hotels, and student residences. The benefits of modular construction are numerous: * **Speed:** Factory-controlled environments eliminate weather delays and allow for parallel construction (site work and module fabrication happening concurrently). A notable example is the **West Swanzey Apartments in New Hampshire**, where an 84-unit affordable housing complex went from a foundation start in February to **80% completion in just 2.5 months** by May 2023 [8]. This accelerated timeline is virtually impossible with traditional stick-built methods. * **Labor Efficiency:** Modular factories can leverage assembly-line processes and automation, requiring fewer total on-site labor hours. This directly addresses the skilled labor shortage by shifting some work to a more controlled, less labor-intensive setting. * **Cost Predictability:** Factory production can lead to more predictable costs as it reduces the impact of on-site labor inefficiencies and unpredictable weather. * **Waste Reduction:** Factory settings often yield less material waste compared to typical construction sites [14], which is particularly relevant in Massachusetts with its strict waste bans [63]. Beyond full modular construction, **panelized methods** are also gaining favor. Prefabricated wall panels, complete with studs and sometimes insulation or sheathing, can reduce on-site framing labor by an estimated **71%** for a typical home [20]. For drywall installers, this could evolve into **pre-rocked wall panels** – sections of drywall factory-attached to the framing, ready for taping and finishing upon arrival. This approach reduces time spent on scaffolding and improves overall precision. The CEO of Avanru Capital, the developer behind the successful Swanzey project, is planning a **$60 million modular factory in New Hampshire** [60], indicating a growing regional commitment to off-site construction.

2.4.2 Technological Integration on Job Sites

Traditional drywall installation is simultaneously benefiting from technological advancements aimed at improving productivity and safety. Contractors are increasingly adopting: * **Automatic Taping and Finishing Tools:** These tools significantly speed up the application of joint compound and mud, improving efficiency and finish quality. * **Laser-Guided Layout Systems:** For precise framing layout, reducing errors and saving time. * **Mobile Elevating Work Platforms (MEWPs) and Panel Lifts:** These mitigate the physical strain of lifting heavy drywall sheets, addressing safety concerns and extending the working careers of an aging workforce. * **Building Information Modeling (BIM):** Digital modeling helps identify conflicts and optimize workflows before construction begins, allowing drywall crews to work more efficiently and reduce costly rework. Massachusetts’ tech-savvy commercial construction sector has been an early adopter of such productivity-enhancing technologies.

2.4.3 Regulatory and Environmental Adaptations

Massachusetts’ regulatory environment is also driving change. The state enforces strict **waste bans** since 2006, prohibiting materials like wood, metal, and “clean” gypsum drywall off-cuts from landfills [21]. This necessitates careful waste sorting and recycling on job sites, adding a layer of management but also incentivizing more efficient material use. With disposal costs around $100 per ton [22], minimizing waste becomes a financial imperative. This regulatory push aligns with the lean principles of modular construction, which inherently generate less waste. Furthermore, new energy codes and upcoming net-zero building mandates mean that drywall installations will increasingly consider environmental factors. This includes specifying materials with lower embodied carbon, using lightweight drywall products, and potentially integrating alternative wall systems like MgO boards or hemp-based panels for niche green projects. While challenges remain, including concerns about quality control for modular builds and the initial investment required for new technologies, the imperative to build “more with less” is driving significant evolution in Massachusetts’ construction practices. The state’s ability to “catch up on this trend” [62] will heavily influence its success in overcoming the housing shortfall.

2.5 Significant Construction Projects Illustrating Market Dynamics

The Massachusetts construction market, including drywall installation, is shaped by a mix of residential development aimed at alleviating the housing crisis and robust activity in key commercial sectors.

2.5.1 Residential Endeavors and Their Challenges

While the state strives to increase housing unit production, large-scale residential projects often face significant hurdles. The **Suffolk Downs Redevelopment in East Boston** serves as a stark reminder of these challenges. Planned as a massive 10,000-unit mixed-use development, it was put on hold in June 2023 due to rising interest rates and construction costs [13]. Only 475 initially planned units proceeded, delaying thousands of potential drywall installation jobs. This instance highlights how even projects with clear market demand can be derailed by unfavorable economic conditions, serving as a critical lesson for developers and contractors to factor in market volatility and flexible phasing strategies. Conversely, the state’s efforts to kick-start housing, such as the Affordable Homes Act that helped initiate 90,400 housing units within 18 months [18], indicate a political will to overcome these obstacles. Small-scale modular housing projects, like the **West Swanzey Apartments (New Hampshire)** [8], offer a model for quicker, more efficient housing delivery that could be scaled up in Massachusetts. These projects demonstrate that while large, traditional residential developments face headwinds, agile and innovative approaches can still deliver much-needed units.

2.5.2 Resilient Commercial Sectors: Biotech and Industrial

In contrast to the fragility of some residential projects, specific commercial sectors, particularly life sciences and industrial facilities, continue to drive significant construction activity in Massachusetts. New England currently has **$23.3 billion in industrial projects underway** [1], with Massachusetts leading in pharma/biotech construction with an estimated **$11.7 billion in active projects** [12]. A prime example is **Takeda’s 16-story, 600,000 sq. ft. R&D center in Cambridge**, expected to complete in 2026 [12]. This complex facility demands extensive and specialized drywall work, including double-studded and double-layered walls for sound damping in labs, fire-rated assemblies, and precise installations to meet stringent cleanroom and vibration criteria. Such projects provide substantial, high-value work for drywall professionals and indicate robust, long-term confidence in the region’s biotech dominance. The continued strength in these sectors shows that overall construction activity is not monolithic. While residential builders might tread cautiously, specialized areas like biotech, infrastructure (new or upgraded utilities, transportation), and institutional construction (universities, hospitals) often proceed due to strategic importance, strong funding, and less sensitivity to short-term market fluctuations. Drywall contractors who have diversified their expertise to include specialized applications required by labs, healthcare facilities, or high-performance office spaces are better positioned to secure a consistent workflow, even if the residential market experiences slowdowns. The coming section will explore the specific trends in drywall materials and installation techniques, further detailing how these market dynamics impact the day-to-day operations and strategic decisions of drywall companies in the Commonwealth.

**Table: Massachusetts Housing & Construction Key Statistics Overview (2020-2025)** | Metric | Data Point (Citation) | Significance | | :—————————————— | :——————————————————————————————————————————— | :————————————————————————————————————————————————————————————————————————————- | | **Housing Units Needed (by early 2030s)** | 220,000 new homes [1] | Represents the scale of the housing shortfall, requiring ~22,000 units/year for stabilization. | | **Housing Permits Issued (2024)** | 14,338 (201/100,000 residents) [2] | 6th lowest per capita nationally (US avg. 281/100k); highlights lagging production despite demand. | | **Net Housing Units Added (2020-Mid 2025)** | 97,656 statewide; 71,135 in Greater Boston [3] | Largest 5-year expansion in decades, but still insufficient to curb high prices and out-migration. | | **MA Construction Unemployment (June 2024)**| 2.5% [8] | Lowest June rate in 17+ years; indicates severe labor scarcity across all trades. | | **MA Average Hourly Wages (early 2024)** | ~$49 [9] | Highest in the nation vs. US average ~$38; reflects tight labor market but increases project costs significantly. | | **Firms Struggling to Hire (2024)** | 94% of U.S. construction firms [6] | Widespread difficulty filling positions, including drywall installers, leading to project delays. | | **Project Delays due to Shortages (2024)** | 54% of contractors [7] | Workforce scarcity is a primary cause of project setbacks, more so than supply chain issues. | | **Drywall Cost Increase (2020-2022)** | ~44.6% (PPI for gypsum building materials) [16] | Volatile material input costs significantly impacted project budgets; eased in 2023 but remains higher than pre-pandemic. | | **Construction Workforce 55+ (2023)** | 30% of residential workers [30] | Aging workforce indicates significant retirement wave, requiring aggressive recruitment and training of new entrants. | | **Modular Construction Share (MA)** | ~2% of new builds [8] | Low adoption rate, but growing interest due to potential for faster delivery and labor efficiency. | | **Tariffs on New Home Costs** | Estimated $7,500 – $10,000 extra per home (due to lumber, steel tariffs) [11] | Adds to overall project costs, impacting affordability and developer margins. | | **Life Sciences Construction in MA** | ~$11.7 billion in active projects [12] | Strong, resilient sector driving demand for specialized construction, including complex drywall installations, even during residential slowdowns. |

Next, we will transition to Section 3: “Drywall Installation Demand & Key Market Segments,” where we will analyze the specific types of projects and sectors driving demand for drywall services in Massachusetts, including residential, commercial, and institutional markets.

3. Labor Market Dynamics and Workforce Challenges

The ambitious goals set by Massachusetts for new construction, particularly in the housing sector, are inextricably linked to the availability and capability of its construction workforce. While the state aims to address a significant housing shortfall and foster growth in key sectors like life sciences, an acute labor shortage presents a formidable and multi-faceted challenge. This section delves into the intricate dynamics of the labor market for new drywall installation projects in Massachusetts, examining critical factors such as persistently low unemployment rates, the resulting surge in wages for skilled trades, the demographic shift characterized by an aging workforce, and the pivotal, albeit sometimes controversial, role of immigrant labor. These elements collectively shape the operational landscape for drywall contractors and developers, influencing project timelines, budgets, and overall feasibility.

3.1. The Pervasive Labor Shortage and its Impact on Project Delivery

Massachusetts’ construction industry is currently grappling with an unprecedented labor crunch, a situation that directly impedes the state’s capacity to meet its aggressive building targets. This shortage is not a new phenomenon, but it has intensified to critical levels, profoundly affecting every facet of construction, including specialized trades like drywall installation. The numbers paint a stark picture: in June 2024, the unemployment rate in the Massachusetts construction sector plummeted to an exceptionally low 2.5%, marking the lowest June rate recorded in over 17 years [7]. Such a low unemployment figure signifies virtually full employment, indicating that nearly every available skilled worker is already engaged in a project. This leaves little room for growth or for easily backfilling positions, making it extraordinarily difficult for firms to expand their capacities or take on new large-scale projects.

The ramifications of this tight labor market are widespread. A national survey conducted in 2024 revealed that a staggering 94% of U.S. construction firms reported having open positions that they struggled to fill [6]. Massachusetts is no exception to this trend; local contractors consistently face chronic openings for critical trades such as drywall installers, carpenters, and electricians. Specifically, 28% of contractors reported having at least 11 unfilled craft positions on their teams as of mid-2024 [6], illustrating a significant deficit in core site labor. This lack of available and qualified personnel translates directly into pervasive project delays. A 2024 industry survey found that 54% of contractors in Massachusetts explicitly attributed project delays to workforce shortages [6]. This figure is particularly telling, as labor scarcity emerged as a more significant cause of construction setbacks than even supply-chain disruptions or material availability, which have dominated industry concerns in recent years. The absence of sufficient skilled workers means that even when materials are readily available, projects can grind to a halt, extending timelines and escalating costs. An example given by Boston-area subcontractors is the need to turn down new work simply because they lack the necessary crews to reliably staff additional projects [46]. This capacity constraint acts as an effective ceiling on the overall volume of construction that can be undertaken simultaneously within the state, directly hindering efforts to address the widespread housing shortfall and commercial development needs.

3.2. Escalating Wages and the Cost Implications

The fundamental economic principle of supply and demand has driven a substantial increase in wages within the Massachusetts construction sector. With a scarcity of skilled labor and high demand for building activity, companies are forced to offer increasingly competitive compensation packages to attract and retain workers. As of early 2024, the average hourly wage for construction workers in Massachusetts reached approximately $48.90 [3]. This figure is not only the highest in the nation—significantly exceeding the U.S. average of roughly $37.70 per hour—but it also represents a consistent upward trend, with wages rising an estimated 5% year-over-year [3]. This rapid wage escalation is a direct consequence of the tight labor market, where competition for talent is fierce among contractors, especially for specialized trades like drywall installation.

For drywall installation contractors, labor represents a substantial portion of overall project costs, often ranging from 40% to 50%. Consequently, sustained wage increases exert immense pressure on profit margins if not accurately forecasted and incorporated into bids. While higher wages are beneficial for workers, drawing more individuals into the trades and compensating them fairly for demanding work, they invariably contribute to the overall increase in project costs. This is a critical factor in why construction in Boston, in particular, is often cited as among the most expensive globally, rivaling cities like New York or San Francisco. The combination of high labor costs, coupled with expensive materials and financing, renders many projects, especially those with tight margins or those aiming for affordability, financially challenging. This dynamic forces developers and contractors to continually re-evaluate the viability of new ventures, sometimes leading to project delays or cancellations, further exacerbating the state’s housing and infrastructure challenges.

3.3. The Aging Workforce: A Demographic Time Bomb

Beneath the surface of immediate labor shortages lies a deeper, more systemic issue: the rapid aging of the Massachusetts construction workforce. This demographic shift portends a significant outflow of experienced talent in the coming decade, further compounding existing labor challenges. As of 2023, approximately 30% of residential construction workers in Massachusetts were 55 years or older [4]. Industry leaders echo this sentiment, observing that the number of workers over 50 has effectively doubled in recent years, while the proportion of younger workers (under 25) has dramatically declined [7].

This demographic imbalance signifies a looming crisis: within the next 5 to 10 years, one in three skilled tradespeople in Massachusetts could retire. The rate of new entrants into the construction trades is currently insufficient to replace these outgoing workers, leading to concerns about the sustainability of the current construction pace, let alone the ability to scale up to meet future demand [4]. The industry has struggled for decades to attract younger generations, partly due to societal pressures that often steer students towards four-year college degrees rather than vocational trades. This has resulted in a “missing generation” of workers in their 20s and 30s who would typically be gaining experience and moving into leadership roles. The absence of these mid-career professionals creates a significant gap in the talent pipeline for supervisory positions, specialized skills, and mentorship of new apprentices. Contractors are increasingly worried about where the next generation of highly skilled individuals, including drywall installers, carpenters, and electricians, will come from [7]. Addressing this issue requires a concerted effort to promote vocational training, apprenticeship programs, and improve the perception of construction careers as stable, well-paying, and technologically advanced.

| Age Group | Share of Residential Construction Workers | Implication |

|---|---|---|

| 55 and Older | 30%[4] | Significant retirement wave expected in next decade. |

| Under 25 | Declining share[7] | Insufficient new entrants to replace retirees. |

| Foreign-born (non-citizen) | 21% (general construction)[7], >50% (some trades)[7] | Critical to labor supply; vulnerable to immigration policy changes. |

3.4. The Critical Role of Immigrant Labor and Its Vulnerabilities

Immigrant labor constitutes a vital, and often indispensable, component of Massachusetts’ construction workforce, playing a crucial role in mitigating the severity of the ongoing labor shortage. In 2023, non-U.S. citizens accounted for approximately 21% of all construction laborers in the state [7], a proportion more than double their share in the overall labor force. For certain specialized trades, this reliance is even more pronounced: over 50% of roofers, masons, and hazardous materials removal workers in Massachusetts are non-citizens, many of whom are believed to be recent immigrants [7]. These workers fill essential roles, particularly in labor-intensive segments of construction, including many aspects of drywall installation, where physical strength and a willingness to perform challenging tasks are paramount.

However, this reliance on immigrant labor introduces a significant vulnerability: the construction industry’s labor supply becomes highly susceptible to shifts in federal immigration policy. Restrictive visa limits or intensified crackdowns on undocumented workers could severely curtail the available labor pool, as evidenced in other regions facing similar challenges [7]. Conversely, supportive immigration policies or pathways to legal employment for foreign-born workers could provide a much-needed influx of talent, helping to alleviate the acute skilled worker gap. The demographics of the construction sector in Massachusetts underscore the need for a pragmatic and stable approach to immigration that recognizes its foundational contribution to the state’s economic and infrastructural development.

This dynamic was brought into sharp focus by a research report from the UMass Amherst Labor Center in 2024, which exposed a disturbing “new business model” prevalent in some residential construction projects. To circumvent high wages and labor costs, certain mid-size drywall and framing subcontractors have reportedly resorted to employing “labor brokers” [1]. These brokers supply crews, often consisting of low-paid, undocumented workers, bypassing traditional payroll taxes, overtime regulations, and benefits. The case of the North Square Apartments in Amherst in 2018-2019 serves as a stark example: a drywall subcontractor with only two official employees ostensibly took on a large project and then subcontracted the actual installation work to a broker. This resulted in dozens of migrant workers experiencing wage theft and exploitation [1]. Such “low-road” practices, once marginal, are now reportedly common in non-union residential projects, undermining ethical contractors who adhere to fair labor laws and standards. This trend not only exploits vulnerable workers but also creates an uneven playing field, jeopardizing the integrity and long-term health of the construction labor market. The revelations have prompted increased scrutiny from regulators and unions, who are advocating for stricter enforcement of labor laws and reforms like joint liability laws that hold general contractors responsible for subcontractor wage theft [1].

3.5. Conclusion and Transition

The labor market for drywall installation and the broader construction industry in Massachusetts is characterized by significant stress. Record-low unemployment, rapidly rising wages, an aging workforce facing imminent retirement, and a critical reliance on immigrant labor—which itself is subject to unique vulnerabilities—collectively create a complex and challenging environment. These factors constrain the industry’s ability to respond effectively to the state’s demand for new housing and commercial development. The pressure to complete projects often leads to undesirable outcomes, from project delays and increased costs to, in some unfortunate instances, the exploitation of vulnerable labor. As Massachusetts strives to build hundreds of thousands of new homes and develop its critical life sciences infrastructure, addressing these multifaceted workforce challenges remains paramount. Without a strategic approach to recruitment, training, retention, and maintaining ethical labor practices, the state’s ambitious construction goals will remain out of reach.

The next section, “Materials and Cost Pressures,” will further explore how rising material costs, inflationary trends, and tariffs compound these labor-related challenges, collectively shaping the financial viability and operational realities of new drywall installation projects in Massachusetts.

4. Material Costs and Supply Chain Volatility

The landscape for new drywall installation projects in Massachusetts has been dramatically reshaped in recent years by unprecedented material cost fluctuations, broader construction material inflation, and the pervasive impact of international trade tariffs. These factors have created a complex and often volatile environment, squeezing developer margins, delaying project timelines, and ultimately contributing to the elevated cost of new construction in the state. While some material prices have stabilized from their pandemic-era peaks, the underlying economic challenges remain significant, demanding innovative strategies and resilient supply chain management from contractors and developers alike.

4.1 The Gypsum Drywall Rollercoaster: Price Surges and Subsequent Stabilization

Few materials experienced such dramatic price volatility during the recent construction boom as gypsum wallboard, the core material for drywall installations. Often considered a staple commodity, its cost became a significant unpredictable variable for contractors. The Producer Price Index (PPI) for gypsum building materials, a key indicator for this sector, vividly illustrates this market turbulence. From 2020 through 2022, the cost of gypsum wallboard and related materials experienced an extraordinary jump, climbing a staggering 44.6% during this two-year period alone[10]. This increase represents one of the sharpest two-year accelerations on record for such a fundamental building input. For drywall contractors, this meant that bids submitted months earlier could be dramatically undercut by rising material costs mid-project, thereby severely eroding profit margins or leading to difficult renegotiations with general contractors and developers.

The impact of this surge can be understood through practical examples. A Boston-area builder, for instance, reported that the standard drywall sheet that might have cost approximately $10 in 2019, consistently escalated to over $14 per sheet at the peak of the material inflation[42]. Considering that even a moderately sized residential project or a commercial fit-out can require thousands of drywall sheets, this seemingly minor per-unit increase translated into substantial material cost overruns, often adding tens of thousands of dollars to a project’s budget. The psychological effect of such unpredictability was also profound; it complicated procurement strategies, incentivized hoarding by some larger players, and intensified competition for available stock.

Fortunately, 2023 brought some much-needed relief and a shift towards stabilization. The PPI for gypsum prices recorded a slight 2.0% year-over-year decrease[10]. This modest decline signaled a cooling market as supply chains gradually caught up with demand, and the frenetic pace of construction eased somewhat in certain sectors. However, despite this recent stabilization, it is critical to note that current drywall prices remain approximately 40% higher than their pre-pandemic levels of 2019. This persistent elevation means that while the acute inflationary pressure seen in 2020-2022 has abated, the new baseline for material costs is significantly higher. This new reality continues to influence overall project viability and necessitates careful cost management and accurate bidding for drywall installation projects across Massachusetts.

4.2 Broader Construction Material Inflation: A Ripple Effect

The trajectory of gypsum wallboard prices was not an isolated phenomenon but rather a reflection of broader inflationary trends across the entire construction materials sector. This widespread inflation created a challenging environment for new drywall installation projects, as the costs of ancillary materials and the structural components integral to framing the drywall also soared.

Consider the volatility in lumber prices, a critical material for the framing that typically supports drywall. After an unprecedented spike, softwood lumber prices, though having experienced a 33% two-year decline, still ended 2023 approximately 22.7% above their 2019 levels[10]. This enduring higher cost for lumber directly impacts the structural budget of a project before a single sheet of drywall is even considered. Beyond lumber, other fundamental inputs also saw substantial increases:

- Ready-mix concrete prices: Jumped 11.2% in 2023 alone[10].

- Steel, insulation, wiring, and fixtures: All experienced double-digit percentage increases since 2020[42].

These collective input cost surges fueled an aggregate construction cost inflation of approximately 17% per year in both 2021 and 2022 for residential projects[10]. This rate far outstripped general inflation during the same period, underscoring the unique pressures faced by the construction industry. While 2023 offered some respite, with average material price increases dropping to a more manageable 1-2%[10], many projects initiated under earlier contracts were still absorbing higher-cost inventory. Projects with longer procurement cycles, such as large commercial or multi-family developments, were particularly vulnerable to these multi-year escalations, as materials bought at peak prices continued to be installed well after market prices began to recede.

The economic impact is stark: builders, faced with these rising costs, have been forced to pass a significant portion onto the end-users. In Massachusetts, this has contributed to the alarming statistic that the median price of a newly built home topped $1 million in 2024[42]. This rising cost base for new construction directly impacts housing affordability and developer margins. Developers operate within a delicate balance of land acquisition, construction costs, and anticipated sale or rental prices. When construction costs rise sharply, without a proportional increase in market demand or a commensurate decrease in other project components, projects can quickly become financially unviable, forcing developers to either scale back, delay, or outright cancel projects. This directly reduces the volume of new drywall installation opportunities in the market.

Table 4.1: Material Price Index Changes (2020-2023)

| Material Category | % Change (2020-2022) | % Change (2023 Year-over-Year) | Contextual Impact |

|---|---|---|---|

| Gypsum Wallboard | +44.6%[10] | -2.0%[10] | Significant direct cost to drywall projects; now ~40% above pre-pandemic levels. |

| Softwood Lumber | Spiked then dropped | Down 33% (2-year decline)[10] | Still 22.7% above 2019 levels; impacts framing and structural costs. |

| Ready-Mix Concrete | N/A | +11.2%[10] | Impacts foundations and structural elements, driving overall project costs. |

| Other Building Materials (Steel, Insulation, Wiring, Fixtures) | Double-digit % increases (since 2020)[42] | Varies (avg 1-2% in 2023)[10] | Contributed to ~17% annual inflation for residential construction in 2021-2022. |

4.3 The Persistent Shadow of Tariffs on Project Costs

Beyond natural market forces and supply chain disruptions, government trade policies in the form of tariffs have compounded the challenge of managing material costs for new drywall installation projects in Massachusetts. These tariffs, imposed on various imported construction materials, act as an additional tax on builders, further escalating project expenses and narrowing already tight developer margins.

The impact of these tariffs is significant and widespread. Estimates suggest that duties on imported lumber, steel, aluminum, and other goods have collectively added between $7,500 and $10,000 to the cost of a typical new single-family home as of 2025[11]. This figure, often considered a hidden cost, directly contributes to the overall affordability crisis in Massachusetts.

Specific examples of tariffs affecting drywall projects include:

- Canadian Lumber: The U.S. has imposed duties of up to 39.5% on Canadian softwood lumber[11]. Given that most drywall installations rely on precisely sized lumber or metal studs for framing, the increased cost of this essential structural component directly inflates the overall cost of a wall or ceiling assembly. Even if a project uses metal studs, the increased cost of lumber often drives up the price of alternative framing materials due to market dynamics.

- Steel: Tariffs of 25% on imported steel[11] directly affect projects utilizing steel studs for framing, often preferred in commercial or high-rise residential buildings for fire resistance and structural integrity. These tariffs also impact the cost of other steel-intensive building components, such as rebar, HVAC systems, and other fixtures, further escalating cumulative project expenses.

The significance of these tariffs is amplified by the fact that approximately 7.3% of all U.S. homebuilding materials are imported[11]. While this percentage might seem modest, it represents critical inputs across various trades, creating a multiplier effect throughout the construction process. For Massachusetts, a state already grappling with some of the highest construction costs nationally, these import tariffs impose an additional burden, making it even more challenging to deliver new housing and commercial spaces at affordable price points.